TYPES OF MARKET STRUCTURE

PERFECT COMPETITION - Describe a market in which there are many small firms all producing homogeneous goods.

MONOPOLY - Monopoly (form Greek monos) alone or single + polein to sell exists when a specific individual or

enterprise has sufficient control over a particular product or services to determine significantly the terms on Wich

other individual shall have access to it.

OLIGOPOLY - Is a market form in which a market or industry is dominated by a small number of sellers (oligopolists).

The word is derived from the Greek for few entities with the right to sell. Because there are few participants in this

type of market, each oligopolist is aware of the actions of the others. The decisions of one firm influence and are

influenced by the decisions of other firms.

MONOPOLISTIC COMPETITION - is a common market form. Many markets can be considered monopolistically

competitive often including the markets for restaurant, cereal, clothing, shoes and service industries in large cities.

Monopolistically competitive markets have the following characteristics

There are many producers and many consumers in a given market and no business has total control over the

market price.

Consumers perceive that there are non-price differences among the competitors’ products.

Producers have a degree of control over price.

Types of Market Structure

1. Monopolistic competition, a type of imperfect competition such that many producers sell products or services

that are differentiated from one another (e.g. by branding or quality) and hence are not perfect substitutes. In

monopolistic competition, a firm takes the prices charged by its rivals as given and ignores the impact of its own

prices on the prices of other. This market structure exists when there are multiple sellers who are attempting to

seem different than each other.

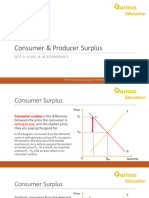

Monopolistic competition in the short run

At profit maximisation, MC = MR, and output is Q and price P. Given that price (AR) is above ATC at Q. supernormal

profits are possible (area PABC).

As new firms enter the market, demand for the existing firm's products becomes more elastic and the demand curve

shifts to the left, driving down price. Eventually, all super-normal profits are eroded away.

Monopolistic competition in the long run

Super-normal profits attract in new entrants, which shifts the demand curve for existing firm to the left. New

entrants continue until only normal profit is available. At this point, firms have reached their long run equilibrium.

Clearly, the firm benefits most when it is in its short run and will try to stay in the short run by innovating, and

further product differentiation.

2. Oligopoly, in which a market is run by a small number of firms that together control the majority of the market

share.

a) Duopoly, a special case of an oligopoly with two firms.

b) Monopsony when there is only a single buyer in a market.

c) Oligopsony, a market where many sellers can be present but meet only a few buyers.

This model suggests that prices will be fairly stable and there is little incentive to change prices. Therefore, firms

compete using non-price competition methods.

This assumes that firms seek to maximize profits

If they increase price, then they will lose a large share of the market because they become uncompetitive

compared to other firms, therefore demand is elastic for price increases.

If firms cut price, then they would gain a big increase in market share, however it is unlikely that firms will allow

this. Therefore, other firms follow suit and cut price as well. Therefore, demand will only increase by a small

amount. Therefore, demand is inelastic for a price cut.

Therefore, this suggests that prices will be rigid in oligopoly

The diagram above suggests that a change in marginal cost still leads to the same price, because of the kinked

demand curve remember profit maximization occurs where MR = MC at Q1.

3. Monopoly, where there is only one provider of a product or service.

A Monopolist is a price maker because he does not face any competitors. Therefore, demand is price inelastic.

A monopolist will seek to maximize profits by setting output where MR = MC

This will be at output Qm and Price Pm.

If the market was competitive the price would be lower and output higher.

Disadvantages of a Monopoly

Green area = Supernormal Profit (AR-AC) Q

Pink area = Deadweight welfare loss (combined loss of producer and consumer surplus) compared to

competitive market.

Higher Prices Higher Price and Lower Output than under Perfect Competition. This leads to a decline in

consumer surplus and a deadweight welfare loss.

Allocative Inefficiency. A monopoly is allocatively inefficient because in monopoly the price is greater than MC. P

> MC. In a competitive market the price would be lower and more consumers would benefit.

Productive Inefficiency A monopoly is productively inefficient because it is not the lowest point on the AC curve.

X-Inefficiency. - It is argued that a monopoly has less incentive to cut costs because it doesn't face competition

from other firms. Therefore, the AC curve is higher than it should be.

Supernormal Profit. A Monopolist makes Supernormal Profit Om * (AR - AC) leading to an unequal distribution

of income.

Higher Prices to Suppliers - A monopoly may use its market power and pay lower prices to its suppliers. E.g.

Supermarkets have been criticized for paying low prices to farmers.

Diseconomies of Scale - It is possible that if a monopoly gets too big it may experience diseconomies of scale. -

higher average costs because it gets too big

Worse products Lack of competition may also lead to improved product innovation.

Charge Higher prices to suppliers. Monopolies may use their supernormal profits to charge higher prices to

suppliers.

Natural monopoly, a monopoly in which economies of scale cause efficiency to increase continuously with the

size of the firm. A firm is a natural monopoly if it is able to serve the entire market demand at a lower cost than

any combination of two or more smaller, more specialized firms.

4. Perfect competition, a theoretical market structure that features low barriers to entry, identical products with no

differentiation, an unlimited number of producers and consumers, and a perfectly elastic demand curve.

In perfect competition there is freedom of entry and exit, and perfect information.

The price set by the industry supply and demand

Firms are price taker; this means their demand curve is perfectly elastic. If they set a higher price no one would

buy it because of perfect knowledge. Therefore, firms have an elastic demand curve.

In the Long Run firms in perfect competition will make normal profits.

Perfect Monopolistic

Characteristics Oligopoly Monopoly

Competition Competition

Number of Many sellers, Many sellers but

producers or each seller each seller not Few Only one

sellers infinitesimal infinitesimal

Identical or Products are

Degree of Some identical,

homogeneous, differentiated but Products have no

product some

product have close substitutes

differentiation differentiated

substitutable substitutes

Degree of control

Some degree of Considerable

over price by No control Some control

control control

producer

Methods of Advertising Promotional and

Advertising

marketing or Market exchange administered public relations

quality rivalry

selling pricing advertising

In agricultural

Nature of Utilities, some

industries; in

presence in Very prevalent Very prevalent highly protected

commodity

economy industries

exchanges

Examples of Rice, corn, Detergents, soap, Cement, steel. Electric power, ice

products coconut, drugs, toothpaste, Paper, metals, plant in small

agricultural junk food, clothes autos, machinery community.

products like designer

jeans, retail trade

How about beer

(San Miguel vs.

Beer Hausen), soft

drinks (Pepsi vs.

Coke vs. 7Up).

These borderlines

of differentiated

competition

involving

oligopoly and

many sellers.